How not to invest in crypto:

How not to invest in crypto:

a personal story about trust and timing, memes and diversification

Part 1: Jake as Early Adopter

A decade or so ago, a couple colleagues persuaded me to buy some bitcoin. I wasn't a hard sell. My affinity for all things shiny and new started young: from playing Civilization on an Apple Classic in New Delhi in the early '90s to typing all my notes on a Palm Pilot at Georgetown Day High School in Washington DC, my extensive and early use of technology did not always make me the most popular kid in class. And while negative responses continued through my status as one of Canada's first Google Glass-holes, my interest in cutting edge technology has not wained.

I am an early adopter - and I use the term loosely as it is no more meaningful than the platitude "futurist" or the currently massively trite "innovative" - with low technology too. Several years ago I began standing at work, or using what is now commonly described as a standing desk. Widely ascribed positive health and productivity benefits, standing desks are now de rigueur but you can bet I was mocked for standing at my double-Ikea desk in 2011 in much the same way I was taunted for typing on my Palm Pilot in 1998 or for using a Palm Treo as a cellphone in 2003.

Among the more interesting aspects of being an "early-adopter" for me are how one can simultaneously be at both ends of the "cool" spectrum. I have almost always been mocked for my early adoption, despite the frequent association of cool-ness with the latest gadgets. And while some currently describe me as a hipster, I have spent most of my life characterized as a geek.

I've often gotten it wrong in jumping on the latest technologies: see my massive home-recorded minidisc collection. And other times I haven't been empowered to act on my prescience: I wanted to buy Bitcoin in 2010 but couldn't find anyone I trusted who also knew how to do so and didn't invest the time to learn myself. Similarly I wanted to invest in Pinterest in 2011 but couldn't find an accredited investor to invest for me.

Back to crypto. With a small group of friends I've been slowly bringing myself up to speed on the current acronym soup of crypto utopianism (DAO, NFT...). From new financial systems to entirely new forms of government, my friend Jay kicked us off with his posts on the sociology and macroeconomics of crypto. More recently, Rohan asked whether “blockchain technologies are a harmful distraction or a much needed opportunity?”

This post is meant to be more personal, a description of how and why I've invested in cryptocurrencies, and why I'm doing so again after losing substantial sums in the past.

The second part of this paper describes some of the investing lessons I fell upon as an early adopter and particularly the importance of diversification as an indication of how much to invest in crypto. In an upcoming post, I wax a bit more poetic about my relationship between trust and technology and how our genetic predisposition to memes might not be the best impulse on which to invest.

Part 2: Diversification and crypto as icing on a cake

Ironically, not too long after I'd given up on investing in bitcoin in 2011, I transitioned out of intellectual property law into tech and the first job I landed was at a Montreal-based startup called Wall Street Survivor. WSS educated its users on finance through paper-trading or gambling without the money.

One of the lessons of this period I’ve retained is that all of investing is gambling, a game of chance, due to the number of variables involved, and human-ness of the system. In this respect, we do our best to bake into this game the risk entailed in a given bet.

The best way I learned to de-risk an investment portfolio was to diversify this risk by investing across multiple risk profiles. In other words, a portfolio should include some relatively low risk investments (e.g. bonds) to balance higher risk investments (e.g. crypto).

One can also view investments that are inversely related as hedges: many think crypto prices will go up as trust in fiat currencies decreases just as financial products with inverse relationships to inflation like public equities and bonds can be hedges.

As I invest back into the crypto market for the third time, I'm trying to take three factors among many others into account, trust, timing and risk. I'm trying to de-risk or increase my trust in the outcomes of these investments by 1. investing the right amount relative to the rest of my portfolio 2. at the right time based on the evolution of the technology behind crypto and the readiness of financial markets for this tech. "Right" here is defined by my comfort level, i.e. the amount of risk I'm willing to take on or the amount of money I'm willing to lose. (insert relevant not financial advice terms)

Vanity Fair's article on the debacle that consumed my second crypto experience, Ponzi Schemes, Private Yachts, And A Missing $250 Million In Crypto: The Strange Tale Of Quadriga is masterful. It reads like an action movie but it also captures why I trusted Quadriga with my Canadian crypto (I had my USD crypto on Coinbase):

In November 2013 Cotten [...] incorporated the Quadriga coin exchange, or QuadrigaCX (named, for reasons that were not immediately clear, after the horse-drawn chariots of the Roman Empire). In a small, inefficient market, Quadriga swiftly distinguished itself. It was the cheapest exchange, the fastest, and, by all appearances, the safest—the first Bitcoin trading platform to hold a money-services business license from FinTRAC, Canada’s anti-money-laundering authority. Quadriga installed a Bitcoin ATM in its office, the second of its kind in Canada, and accepted gold by the ounce, which could be dropped off in person. Investing with Quadriga was even patriotic: “People like the fact we’re located in Canada,” Cotten told an interviewer, a point he often emphasized. “They know where their money is going.”

Little did I know Quadriga's founder would be found dead only a couple years after I'd bet on it as the safest place to store crypto value in our slow-moving country.

So this time round I'm trying to apply some of the lessons about diversification from my time at Wall Street Survivor to my investments. This is the clearest and most easily applicable lesson I hope to convey:

no matter how much you invest in crypto, ensure your liquid investments or capital is sufficiently diversified to de-risk any particular asset class or investment.

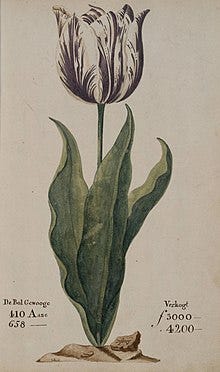

Crypto is suffering from the same frothiness as Tulip Mania: people are buying in the dip but not selling at the top - so people just keep doubling down. As Wikipedia explains, “the term "tulip mania" is now often used metaphorically to refer to any large economic bubble when asset prices deviate from intrinsic values.”

Tim Nash, of Good Investing, described a psychology of all or nothing right now in crypto, from Gamestop or AMC, to Dogecoin or Crypto Kitties or NBA top shot, investors seem proud to be all in (Doge to the moon!) which is counter to one of the most fundamental rules of investing, diversification.

I'll conclude with a couple more paragraphs from the story of how I lost most of my second crypto fortune:

"A couple of years after graduation, Cotten moved to Vancouver and joined a clubby community of entrepreneurs who had become enamored with Bitcoin. He attended meetups at coffee shops and dorm rooms, organized by a core group of about 10 people, who called themselves the Vancouver Bitcoin Co-op. Most of these early acolytes were drawn to the digital currency’s libertarian ethos, its promises of decentralization, transparency, speed, and independence from governments and financial institutions. Bitcoin would enable more than two billion people who lacked access to banks to send and receive payment; it would offer stability to citizens of countries with chaotic currencies; it would eliminate all banking fees.

Cotten knew the catchphrases and the talking points, but he seemed most interested in Bitcoin’s speculative possibilities. The first Bitcoin block was created on January 3, 2009, and the currency gained economic value on May 22, 2010, a date enshrined in Bitcoin lore as “Pizza Day,” when a Florida man paid someone in England 10,000 Bitcoins to order him two pizzas from Papa John’s. The pizzas cost about $25, setting the price of a Bitcoin at one fourth of a penny. (At press time those pizzas would be valued at $82,373,500.) With that, Bitcoin became like any other form of currency, a mass delusion: It’s value derived from the belief that it had value."

In part 2 of this series I’ll go into more depth on Tim’s theory of diversification while continuing to question the merits of this crypto craze.

Excellent post! If you haven't heard it already, I recommend the CBC podcast 'A Death in Cryptoland' by Takara Small on the same topic.